The feeling is strong, I get it. You graduated college and started making good money. You want to show that you’ve made it, so you buy that sweet new BMW or Tesla. After all, you feel confident you can keep up with the payments on your steady monthly income. While buying the flashy car might seem like a fine decision, this is one of the most common car buying mistakes in your 20s. And it’s one that can set you back in so many ways. In this article, we’ll break down why buying an expensive car in your 20s is a mistake many come to regret, and what you can do instead.

No one cares you have a nice car

It might seem like having a nice car is the ultimate status symbol. It says you’re a working professional. It signals you can afford the nicer things in life. It shows you’re successful. In your 20s, it’s easy to overestimate how much people care but the truth is, they usually don’t. They’ll see your nice car, be impressed for 2 minutes, then go back to wondering what they’re going to eat for lunch.

Even if your car does impress strangers, does that really matter? That fleeting admiration doesn’t cover your monthly car payment. And for your friends, they’ll be more impressed by your character than your car. The point is, impressing people at the cost of $1000 a month just isn’t worth it. Objectively it’s doing nothing for you except crippling your finances and your future.

How Car Payments Kill Your Wealth in Your 20s

Your 20s are the most powerful time to invest your money. Compound interest turns small investments into massive returns, and your 20s give you the longest runway to build that growth. Instead of paying that expensive monthly car payment, you could invest that money and watch it grow to six figures by your 30s.

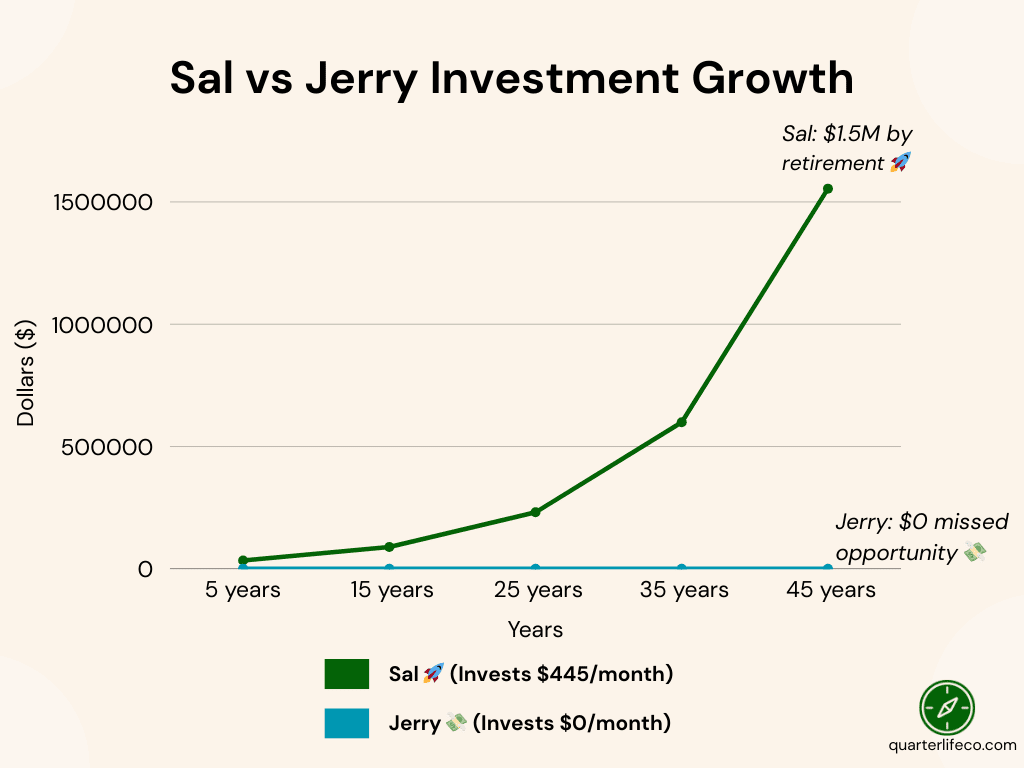

Let’s do a thought experiment. Both Sal and Jerry just graduated college and got their first big boy jobs with their first big boy paychecks. Sal buys a $20,000 Toyota. With a 60 month loan he pays $387/month. Jerry chooses a $50,000 BMW. Same loan term but his payment is $832/month. That’s a difference of $445 per month for 5 years! For the sake of the thought experiment, let’s say Sal puts that extra $445 he has into the market, which generates an average of 10% returns a year. Reference our article to see how you can invest like Sal.

After 5 years: ~ $35,000

After 25 years: ~ $230,000

After 45years (retirement): ~ $1.5million

This is all just from the $445 a month he saved for five years during his early 20s. Meaning with his purchase of a BMW, Jerry lost out on nearly $1.5 million of future wealth for a car he never even needed. Luxury car payments are one of the biggest financial mistakes in your 20s because they cost you not just money, but decades of future compound growth.

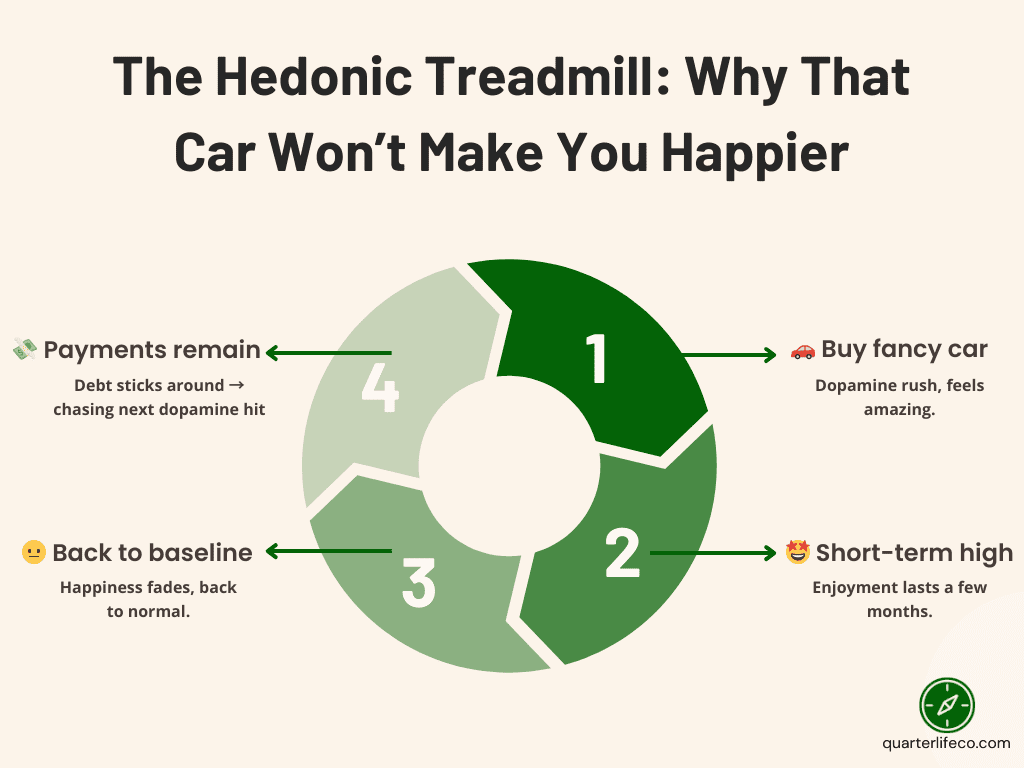

The Hedonic Treadmill: Why That Shiny Car Won’t Make You Happier

Let’s drop some evolutionary psychology into this. The hedonic treadmill is the idea that humans quickly return to a baseline level of happiness after experiencing a positive (or negative) event. In other words, we are constantly chasing more pleasures to capture that “happy” feeling again. This applies directly to buying a new car. You feel amazing for a few months after purchasing the car. But eventually, your brain normalizes it and the excitement fades. Now your baseline happiness is the same as before you bought the car, except you have a $832 month bill you have to keep up with. That’s the hedonic treadmill, short term highs that material possessions will never satisfy.

That dopamine hit you get from the fancy car? It doesn’t last. The worst part? While the happiness fades, the financial hit sticks around for decades. So go with the cheaper car. It won’t make you any less happy and your future self will thank you.

A Car Payment is a Freedom Payment

In your 20s, you want to have as much flexibility as possible. This gives you the ability to hop jobs, travel the world, or even quit your job to start a dream business. But when you lock yourself in to a big financial responsibility like an expensive car, that flexibility shrinks.

A car payment ties you down. You can’t quit. You can’t move. All because of this responsibility you took on. If you had a 10k used car instead, you could sell it off and make your next move easier. In your 20s, freedom is worth way more than the fancy car.

From personal experience, one of the best decisions I made was buying a used Toyota Corolla and paying it off right away. Because I didn’t have monthly payments, I was able to walk away from a six figure job to pursue something more fulfilling. And it’s ultimately what gave me the freedom to join the Peace Corps. I didn’t need to keep making big money just to keep up with a car loan.

As you progress through your 20s, you’ll realize that while the money is great, freedom is everything. Your 20s are such a rare time when you have no responsibilities and can explore freely. Don’t put the unnecessary burden of an expensive car payment on yourself and cripple the decisions future you wants to make.

Cars Are One of the Worst Assets You Can Own

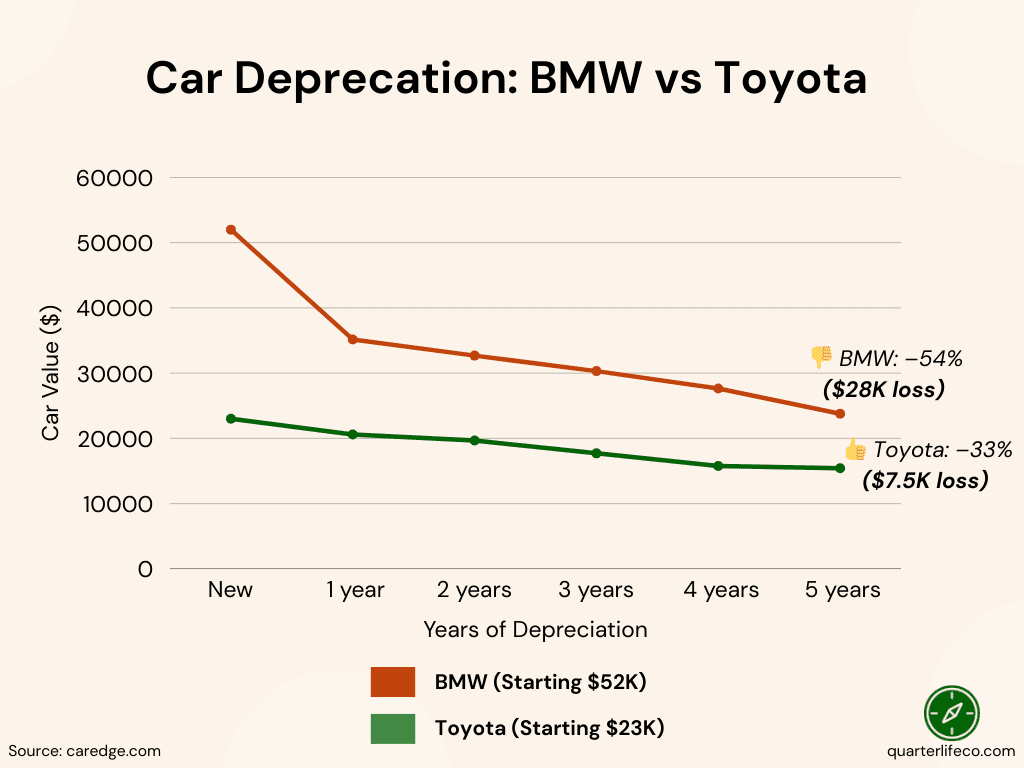

Cars lose value the moment you drive them off the lot and fancier cars even faster. After just 5 years, a BMW only holds about 54% of its value. A cheaper car like a Corolla holds more value at around 33% but it’s still a big drop. This is exactly why buying used is smarter. Let the previous owner eat the massive depreciation hit.

Here’s the bottom line. In your 20s you want to buy assets, like mutual funds, that build your wealth over time. A car does the opposite. All you’re doing is losing money. There’s absolutely no financial upside. Along with depreciating in value, fancier cars come with higher insurance, premium fuel and expensive repairs. It’s just one more example of how a fancy car drains your money and future wealth.

Conclusion: Buy the Cheap, Used Car.

In your 20s, the goal isn’t to impress. It’s to build your future through money and meaningful experiences. Locking yourself into a commitment with a fancy car limits both. You might think a luxury car is what success looks like, but the real success is financial freedom and control over your life. A car robs you of both. While the car you drive doesn’t define your success, the choices you make now do. So buy the used car and live your life richly in all the ways that actually matter.

Summary

- 🚫 Expensive cars in your 20s drain wealth and freedom.

- 💸 A BMW loses $28K in 5 years. A Toyota only $7.5K.

- ⏳ Your 20s are the best time to invest and grow money.

- 🌍 Freedom and flexibility matter more than status symbols as a young adult.

Article FAQ

Leasing can look attractive because of lower upfront costs, but it’s usually not a smart financial move in your 20s. You’re paying for temporary use with no equity, and penalties to break the lease can make it even more expensive if your situation changes.

Almost always the better choice is a used car. With new cars, as soon as you drive it off the lot, the value of the car tanks. Buying used ensures that the previous owner eats the massive deprecation first and is like buying a car on sale!

An expensive car is not a true asset. Cars lose value the moment you drive them off the lot and continue to depreciate every year, especially luxury models. Instead of building wealth, they drain it through payments, insurance, fuel, and repairs. Real assets are things like investments, property, or businesses that grow in value over time. All a car does is lose value over time.

Many young professionals buy luxury cars to signal success or reward themselves for a new paycheck. But the excitement fades fast (the hedonic treadmill), and the payments stick around. Often, that money could’ve grown into hundreds of thousands of dollars if invested.

Beyond the monthly payment, the biggest hidden costs are insurance, maintenance, and depreciation. A luxury car comes with much higher insurance premiums and repair bills, while also losing value faster than a reliable economy car.