A credit score in your 20s is like a financial report card. It’s a prediction of your credit worthiness. Lenders like banks and credit card companies use it to gauge the likelihood an individual will pay back borrowed money. In your 20s, this number can make your first big steps into adulthood much easier, like whether you get approved for your first apartment, whether your first car loan has a good interest rate, or even the quality of your first credit card.

Starting to build your credit in your 20s will also help substantially as you progress through life, whether you want a loan for your new business or you want to buy a house eventually. This guide will break down why it’s so important to build your credit in your 20s, how to check your credit score, and most importantly, methods you can employ to get that number up.

Why is it important?

First Apartment: Most landlords check credit scores as part of the rental application process.

Qualifying For a Credit Card: A higher credit score equals a higher chance of getting approved for credit cards with better perks and rewards.

Cost of Borrowing: A higher credit score increases your chances of qualifying for lower interest rates on loans, like for your student loans or car loans.

Insurance Rates: Insurance companies can use your credit score to determine premiums.

Future Big Purchases: Setting up your credit in your 20s makes it easier to get lower interest loans for a home or business you want to start in the future.

And More!

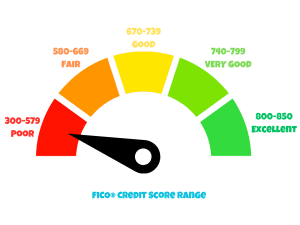

The chart below gives a good idea of what qualifies as a good (and not so good) credit score. Keeping this score as high as you can will help you out a ton in your financial journey.

How to Check Your Credit Score

With a credit score, there’s what’s known as a soft inquiry and a hard inquiry.

The methods of checking your credit score outlined in this guide constitute as soft inquiries. This is when you check your own credit or a company pre-approves you for a credit card or loan offer. This method doesn’t affect your credit score.

A hard inquiry is a hard pull on your credit score. This happens when you actually apply for a new credit line like a car loan, credit card, or mortgage. This can temporarily lower your score by a few points, and typically stays on your report for about 2 years. Too many of these in a short time can raise some flags to lenders, but a few is totally fine!

There’s two types of scores you can use to track your credit health.

FICO Score – Most widely used credit score by lenders, banks and credit card companies.

Vantage Score – Another score to measure credit, but used less by lenders and not as useful of a way to track compared to your FICO Score. This was created by the three major credit bureaus: Experian, Equifax and Transunion.

Both scores measure your credit health, but there are important differences between FICO and VantageScore. Your FICO Score is the official number most lenders pay attention to when deciding things like loans or credit cards. VantageScore, on the other hand, is free and easy to check, and still gives a solid picture of your credit standing. What makes these scores different is the algorithms they use. So, sometimes your VantageScore will match your FICO Score, but other times it could be 20-50 points off. Still, VantageScore is a great tool to use considering how easy it is to check. Think of the VantageScore like your fitness watch. Not official health data, but it gives you a good idea of where you stand. The FICO Score is the official results after your visit to the doctor’s office.

In this guide, we’ll walk you through how to access both, so you can track the progress of your credit journey easily (VantageScore) while still knowing the number lenders care about most (FICO Score).

How To Check Your VantageScore

Make an Account at CreditKarma

Go to CreditKarma.com and sign up for an account.

Your account at CreditKarma will give you access to great information about your credit and financial history. One important thing you’ll be able access is your VantageScore through two of the three major credit bureaus (Transunion and Equifax).

Other information you’ll be able to access includes:

- Credit Report (from Equifax & TransUnion)

- Credit Monitoring & Alerts (notifies you of significant changes)

- Credit Score Breakdown (shows factors affecting your score)

- Credit Score Simulator (see how actions impact your score)

- Personalized Recommendations (credit card, loan, and financial product suggestions)

- Account & Loan Tracking (monitor credit accounts and loans)

- Dispute Errors (dispute mistakes on your credit report)

- Basic Identity Monitoring (alerts for suspicious activity)

- Financial Tools & Calculators (calculators for payments, debt, etc.)

While lenders are still only recently starting to use VantageScore, and FICO Score is still the top metric to many, access to all these features in CreditKarma is totally free and doesn’t hurt your credit by checking them, since it’s what’s called a “soft inquiry”.

How To Check Your FICO Score

There’s so many ways to check your FICO Score. Since this is Quarter Life Co., we’ll give the simplest and free way: Experian.com

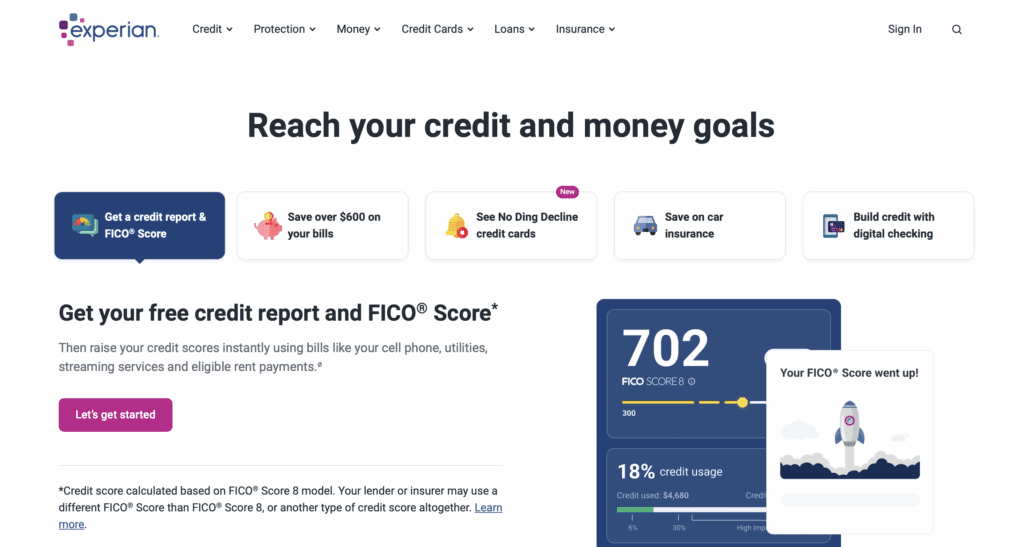

Make an Account at Experian.com

The simplest way to check your FICO Score is by creating a free account at Experian.com. Here you can see your Experian-based FICO Score 8, which is one of the most widely used versions lenders look at. It’s completely free and checking it only counts as a soft inquiry so it won’t hurt your score.

Keep in mind, the FICO Score you see at Experian won’t always be the exact number a lender would pull. This is for a variety of reasons. There’s different bureaus so a lender could pull your FICO from Equifax instead of Experian, for example. Also, FICO has multiple versions (FICO 8, FICO 9, Auto Score, etc.), and lenders use different ones depending on the type of loan.

With that being said, this FICO score is still more accurate than a VantageScore, defining accurate as closer to what the lenders actually look at. Still, we use Credit Karma to check the VantageScore because the website is better for day to day tracking and has more in depth information of how your credit score is progressing.

How To Improve Your Credit Score

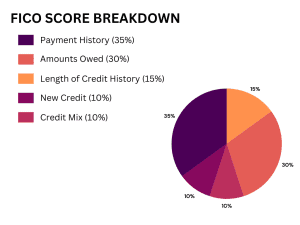

Since the FICO Score is the one most lenders look at, let’s deep dive how to improve that score. Look at the chart below to see the percent contribution of the different factors that go into your FICO credit score.

If you can improve these following areas, it will raise your credit score, giving you the advantages of great credit.

- Payment History: Making consistent on-time payments improves your credit score more than any other factor. This includes completing a loan payment every month, and paying your credit card bill every month. Note that while you can pay the minimum on the credit card and it won’t directly hurt your credit, this isn’t a smart strategy as you can accrue interest on the amount you don’t pay, as well as increase your credit utilization which affects the “Amounts Owed” portion.

- Amounts Owed: If the current amount of money you owe on your credit lines is high, this can tell banks you might be overextended, meaning you are at higher risk of defaulting. To improve this portion, pay your credit bill every month and clear any outstanding debts. Another key part of this section is credit utilization, which is the ratio of your credit card balances to your credit card limits. For example, say you have one credit car with a $5000 limit. If you consistently carry a balance of $2000 on that card, your utilization would be 40%. That’s considered high and can drag down your score. It’s recommended to keep that percentage at least below 30% (10% is the most optimal). You can do that by paying your balance off in full every month, requesting a higher credit limit, or making multiple payments were month on you credit card.

- Length of Credit History: This covers how long your credit account has been established. This includes the age of your oldest account, the age of your newest account and the average age of all your accounts. If you have an old credit card that you don’t use much anymore, still keep it open as this is great for your credit score.

- New Credit: When you apply for new credit, there is a hard inquiry on your credit information for lenders to determine if they’ll approve your credit request. This very slightly lowers your credit score for a temporary period (think 1 to 2 years).

- Credit Mix: A credit mix such as credit cards as well as loans contributes to raising this portion, since it shows responsibility with different types of lending.

Article FAQ

Yes. Even if you’re not using them, keeping old credit cards open improves the length of your credit history, which is 15% of your score.

Credit utilization is how much of your available credit you’re using. For example, say your credit card has a limit of $10,000 and you have $4,000 owed on it right now. That means your credit utilization is 40%. To improve this, pay off the debt or ask your credit card compay to increase your limit. This would in turn lower the utilization ratio. The credit card company increases the limit to $20,000, your utilization is now at 20%.

There’s two things you can focus on in the short term to build credit fast. The first is make sure you don’t have any outstanding debts on your cards and clear it up as fast as possible. If you can’t clear all of it, then ask for a higher credit limit so you lower your utilization rate.

If you see a financial error on a site like Credit Karma, such as you showing a debt you don’t believe you owe, you can dispute it with the credit bureau.

Typically, a credit score of 670 or higher on the FICO scale is considered good credit. Scores of 740+ are very good and 800+ is excellent!

If you check through the resources provided in this article, the answer is no. These would be called soft inquiries and don’t affect your credit. Only hard inquires such as when you apply for loans or credit cards can temporarily lower your score.

Your 20s are prime time to start building your credit history. You probably don’t need a mortgage or business loan yet, but learning how to build your credit score in your 20s will prepare you for those big future milestones. At the end of the day, a credit score is just a measure of how responsibly you handle borrowed money.

If you consistently pay your balances on time, keep you credit utilization low, and avoid taking on unnecessary debt, you score will soar. Over time, that better credit score will unlock better credit cards, lower interest rates on loans, easier approval for apartments, and a host of other advantages. The earlier you start, the more time you’ll be able to reap the rewards of great credit.